How to Save Money on ITR Filing: Smart Tax Deductions Every Indian Must Know

Most Indians overpay their income tax by ₹20,000 to ₹50,000 every year simply because they don’t know which deductions to claim.

Filing your Income Tax Return (ITR) doesn’t have to mean giving away a big chunk of your salary to the government. With the right knowledge, you can legally reduce your tax bill and keep more money in your pocket. This guide shows you exactly how to save money when filing ITR in India, with real examples and practical tips that actually work.

What You’ll Learn

- How to claim up to ₹1.5 lakhs deduction under Section 80C with proper investments

- Why health insurance under Section 80D can save you ₹25,000 to ₹75,000 extra

- The difference between old and new tax regimes and which one saves you more money

- Common ITR filing mistakes that cost Indians thousands in penalties and lost deductions

- How to use NPS, home loan interest, and HRA to further reduce your taxable income

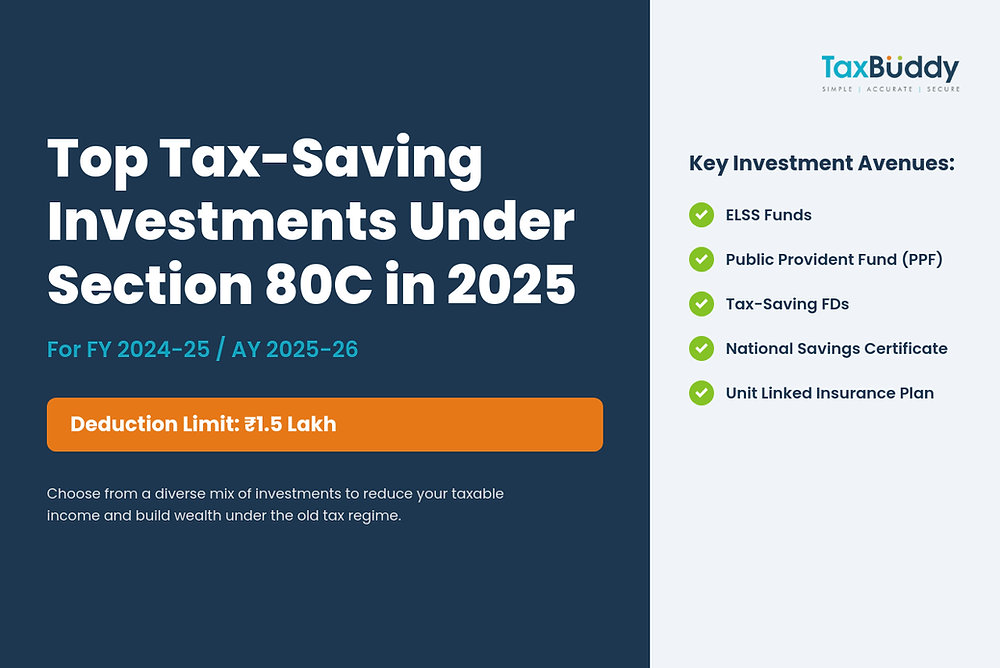

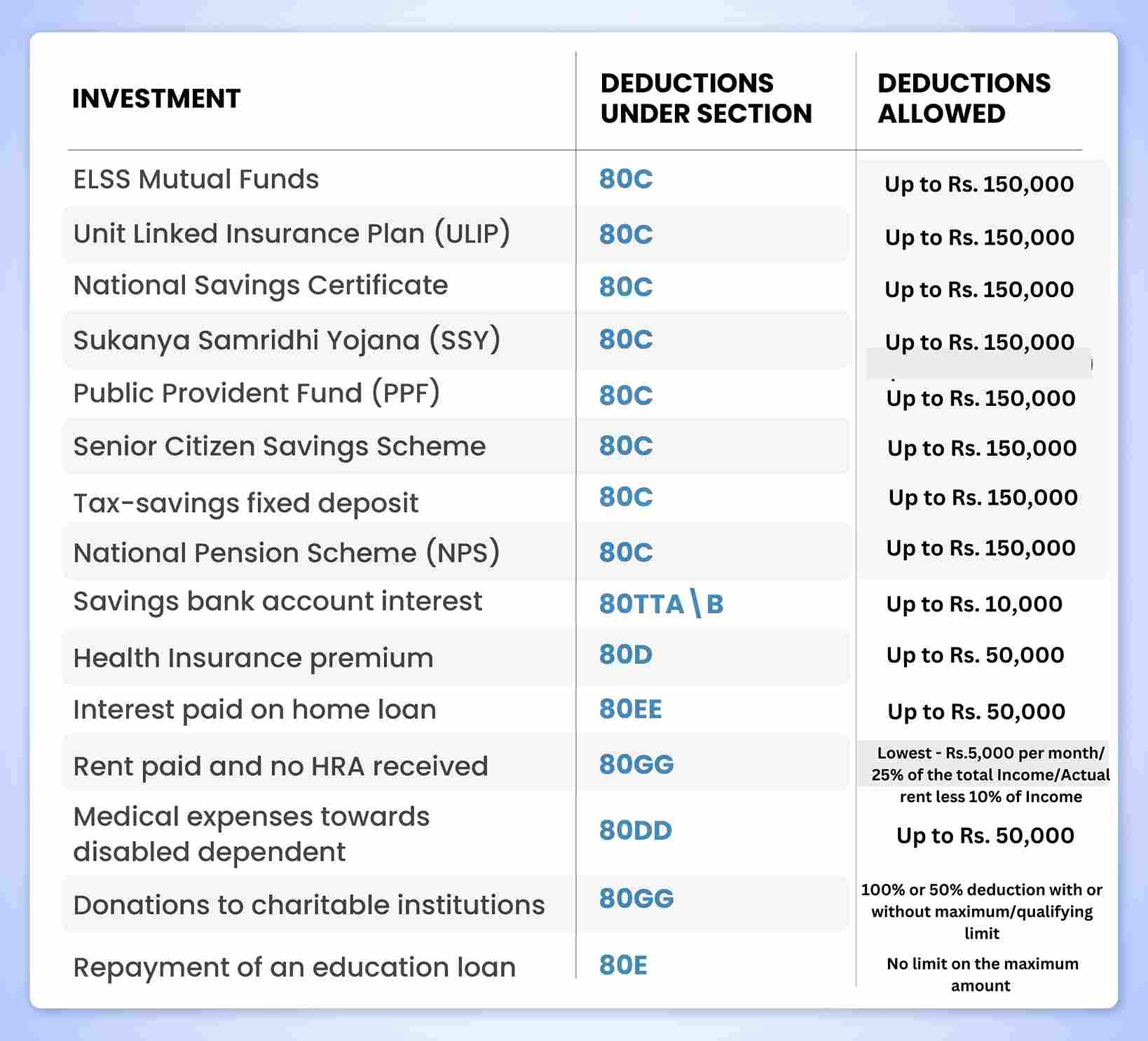

Section 80C: Your ₹1.5 Lakh Tax Saving Bucket

Section 80C is the most popular way to save tax in India. Every individual and Hindu Undivided Family (HUF) can claim deductions up to ₹1.5 lakhs per year. This means if you invest wisely, you can reduce your taxable income by ₹1.5 lakhs instantly.

Here are the best options that qualify for 80C:

- Public Provident Fund (PPF) — Safe, government-backed, 7.1% interest

- ELSS Mutual Funds — 3-year lock-in, potential for higher returns

- Life Insurance Premiums — Protection plus tax saving

- 5-Year Tax Saver FDs — Bank deposits with guaranteed returns

- National Savings Certificate (NSC) — Post office scheme, secure

- Sukanya Samriddhi Yojana — Best for girl child education savings

- Home Loan Principal Repayment — If you have a housing loan

💡 Real Example: If your taxable income is ₹8 lakhs and you invest ₹1.5 lakhs in PPF or ELSS, you pay tax only on ₹6.5 lakhs. At 20% slab, you save ₹30,000 in tax immediately.

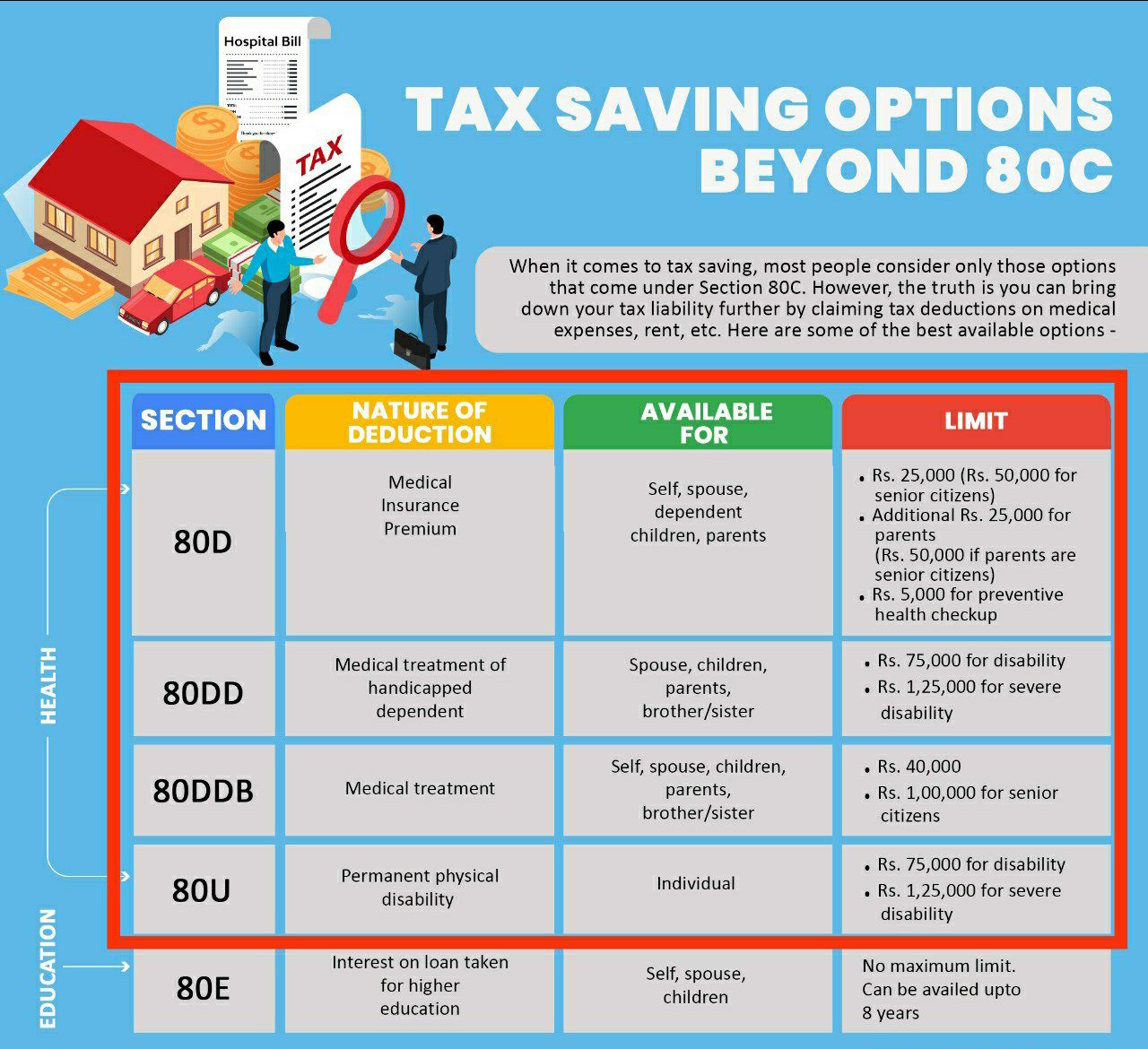

Section 80D: Save Tax on Health Insurance Premiums

Many people forget to claim this deduction, but Section 80D can save you up to ₹75,000 depending on your age and family structure. This is separate from 80C, so you get this benefit on top of your ₹1.5 lakh investment deduction.

Here’s how it works:

- For self, spouse, children: Up to ₹25,000 (₹50,000 if you’re above 60)

- For parents: Additional ₹25,000 (₹50,000 if parents are senior citizens)

- Preventive health check-up: Extra ₹5,000 within the above limits

So if you pay health insurance for yourself (₹25,000) and your senior citizen parents (₹50,000), you get a total deduction of ₹75,000. According to Economic Times, this is one of the most commonly missed deductions.

Step-by-Step: How to File ITR and Maximize Savings

Follow these steps to ensure you don’t miss any deductions and file correctly:

- Choose Your Tax Regime First — Compare old vs new regime. Old regime allows 80C, 80D deductions. New regime has lower tax rates but only ₹75,000 standard deduction plus NPS employer contribution.

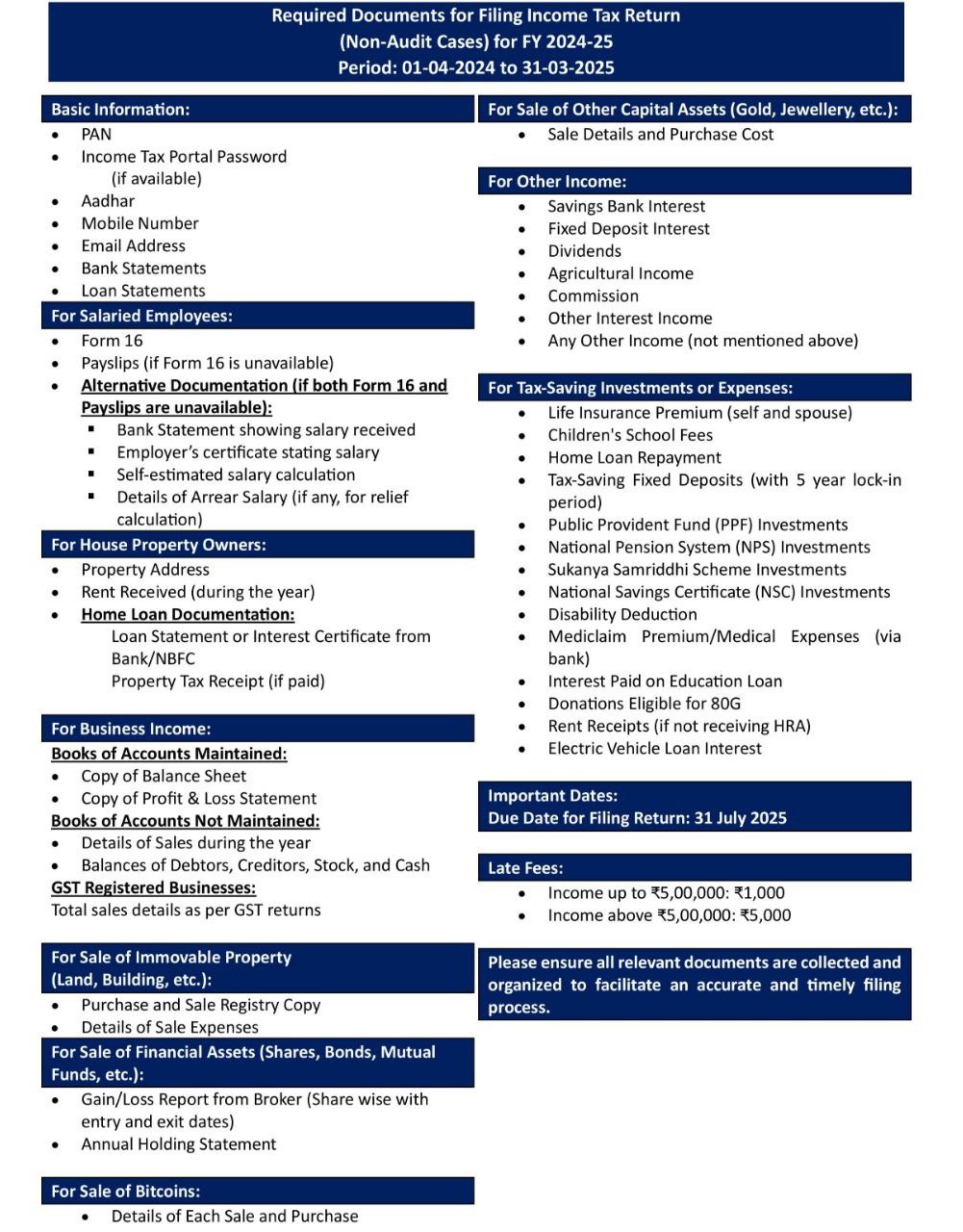

- Collect All Documents — Form 16 from employer, bank statements, investment proofs, home loan certificate, rent receipts, health insurance premium receipts.

- Check Form 26AS and AIS — Verify all TDS deducted matches your records. Many people face notices because of mismatches here.

- Calculate All Income Sources — Include salary, interest from savings (even if below ₹10,000), FD interest, rental income, capital gains, freelance income.

- Claim Every Eligible Deduction — Don’t just stop at 80C. Check 80D, 80E (education loan), 24(b) (home loan interest), 80TTA (savings interest up to ₹10,000).

- File Before Deadline — Due date is July 31 for most individuals. Late filing attracts penalty up to ₹5,000 under Section 234F.

- Verify Your Return — E-verify within 120 days using Aadhaar OTP or net banking. Without verification, your return is invalid.

Old vs New Tax Regime: Which Saves You More?

This is the biggest confusion for Indian taxpayers. The new tax regime has lower slab rates but you lose most deductions. The old regime has higher rates but allows 80C, 80D, HRA, home loan benefits.

Choose old regime if:

- You claim full ₹1.5 lakh under 80C

- You pay home loan EMI (Section 24)

- You get HRA and live in rented house

- You have health insurance for family and parents

Choose new regime if:

- You don’t have many investments or loans

- Your income is below ₹12 lakhs and you want simplicity

- Your employer contributes to NPS (14% of basic is tax-free here vs 10% in old)

Common Mistakes That Cost You Money

- Not reporting all income — Even savings account interest must be reported. If above ₹10,000, it’s taxable. Below that, claim 80TTA deduction.

- Missing the deduction deadline — You cannot claim 80C investments made after March 31 for that financial year.

- Wrong ITR form selection — Salaried people with capital gains cannot use ITR-1. Using wrong form leads to defective notice.

- Ignoring Form 26AS — If TDS is deducted but not reflecting in 26AS, you won’t get credit. Always reconcile before filing.

- Not verifying return — Filing is incomplete without e-verification. Many people miss this and their return becomes invalid.

⚡ Pro Tips That Actually Work

- Start tax planning in April, not March — Last minute investments often lead to poor choices. Start SIP in ELSS from April itself.

- Split 80C between PPF and ELSS — PPF gives safety, ELSS gives growth. Don’t put everything in one basket.

- Buy health insurance before March 31 — Premium paid in the financial year counts for that year’s 80D deduction.

- Keep rent receipts even if HRA is small — Even ₹2,000 per month HRA exemption saves ₹7,200 in tax over the year.

- Use NPS for extra ₹50,000 benefit — Section 80CCD(1B) gives additional deduction over and above 80C. This is exclusive to NPS.

Beyond 80C: Additional Ways to Save Tax

Smart taxpayers don’t stop at Section 80C. Here are more legal ways to reduce your tax:

Home Loan Interest (Section 24): If you have a home loan for self-occupied property, claim up to ₹2 lakhs interest deduction. For let-out property, there’s no upper limit on interest claim.

Education Loan (Section 80E): Interest paid on education loan for self, spouse, or children is fully deductible for up to 8 years. No upper limit on the amount.

Savings Account Interest (Section 80TTA): Get ₹10,000 deduction on interest from savings accounts. For senior citizens, 80TTB gives ₹50,000 on FD and savings interest.

Donations (Section 80G): Donations to PM Relief Fund, National Defence Fund give 100% deduction. Others give 50% deduction.

Frequently Asked Questions

📌 Quick Summary

Saving money on ITR filing is about knowing which deductions you qualify for and claiming them correctly before the deadline.

Maximize Section 80C (₹1.5L), don’t forget Section 80D for health insurance (up to ₹75K), and choose the tax regime that fits your financial profile.

Start collecting your documents now, file before July 31, and always e-verify your return to ensure it’s processed.

{kind=link}